For high-revenue founders, scaling operations is a constant balancing act between aggressive growth and liquidity management. Acquiring heavy machinery, expanding commercial fleets, or upgrading enterprise technology requires substantial capital expenditure. Traditionally, the cost of these major assets had to be recovered slowly over multiple years through complex depreciation schedules.

However, the U.S. tax code provides a powerful mechanism to bypass this slow recovery: the Section 179 deduction. By understanding and strategically leveraging this deduction, founders can acquire the fixed assets they need to scale, achieve a massive reduction in their corporate tax liability, and protect their cash reserves for core operations.

What is the Section 179 Deduction?

Section 179 of the tax code is an election that allows you to recover all or part of the cost of qualifying property by deducting it entirely in the year you place the property in service. Instead of capitalizing the cost of a new piece of equipment and depreciating it incrementally over a five, seven, or ten-year recovery period, the IRS allows you to deduct the full purchase price from your business’s taxable income upfront.

What is in it for you? The strategic advantage here is immediate cash flow relief. By lowering your taxable income in the exact year you purchase and deploy the equipment, your business realizes substantial tax savings immediately. This allows you to aggressively scale your operational capabilities without permanently draining your liquid cash reserves, keeping that capital free for payroll, marketing, and emergency bridging.

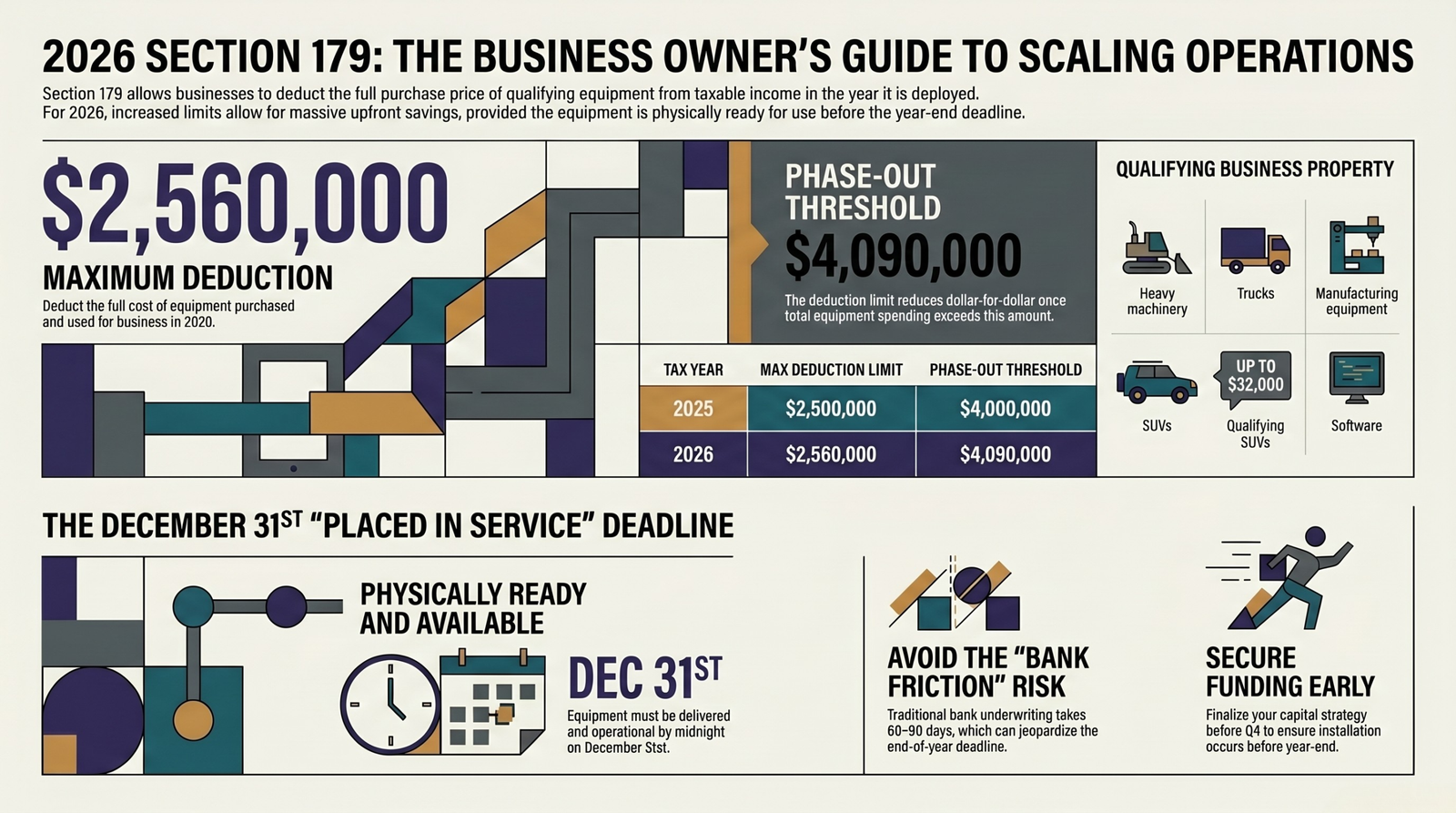

The 2026 Tax Limits High-Revenue Founders Need to Know

The IRS strictly governs the total amount a business can deduct, and these figures are adjusted for inflation. To ensure this benefit primarily stimulates small and medium-sized enterprises, the code institutes specific limits and phase-out thresholds.

If you are planning your capital expenditures for the upcoming year, you must adhere to the 2026 limits:

- The Maximum Deduction Limit: For tax years beginning in 2026, the absolute maximum Section 179 expense deduction you can elect to take is $2,560,000.

- The Investment Phase-Out Cap: The IRS reduces your 2,560,000limitdollar−for−dollarbytheamountthatyourtotalcostofSection179propertyplacedinserviceduringtheyearexceeds∗∗4,090,000**. Consequently, if your business purchases $6,650,000 or more in qualifying equipment during 2026, the deduction is completely phased out.

To take advantage of these limits, the property must be acquired by purchase and must be used more than 50% for business purposes in the year you place it in service. Eligible property generally includes tangible personal property like heavy machinery, manufacturing equipment, business vehicles, and off-the-shelf computer software.

The Timeline Risk: How Bank Friction Can Cost You the Deduction

While the financial benefits of Section 179 are profound, realizing those benefits requires strict adherence to the IRS timeline. To claim the deduction for a given tax year, the equipment must actually be “placed in service” before the end of the year. The IRS defines “placed in service” as the date the property is physically ready and available for its specific use in your trade or business. Buying the equipment in late December and leaving it in a box or awaiting installation does not qualify.

This strict December 31st deadline introduces a severe operational risk for founders relying on traditional banking channels.

When you apply for a standard commercial equipment loan, institutional banks often require 60 to 90 days just to complete the underwriting process. They typically demand endless documentation, strict lending covenants, and mandatory personal guarantees where you must pledge your home or personal real estate as collateral.

This archaic bank friction is not just an administrative headache; it is a direct timeline risk. If the bank takes two months to approve your funding, you may not be able to finalize the purchase, take delivery, and physically place the machinery in service before the December 31st deadline. If you cross into January 1st, you lose the ability to deduct that purchase against your current year’s tax liability.

The Alternative Capital Strategy

To bypass this institutional friction, the top 1% of high-revenue founders increasingly rely on alternative, non-bank capital.

Alternative commercial finance operates on an entirely different timeline, evaluating the real-time cash flow and health of the business rather than requiring mountains of personal tax returns and personal guarantees. By utilizing agile capital solutions, founders can secure their equipment financing rapidly—often in a matter of days. This speed completely removes the timeline risk of traditional banking, ensuring that the enterprise can acquire, install, and place the required equipment in service with plenty of time to secure the Section 179 tax break before the year closes.

Next Steps: Finalize Your Capital Strategy

Maximizing your equipment financing and tax deductions requires proactive planning. Do not wait until the end of the year to discover that slow underwriting will cost you a massive tax break. We advise all business owners to speak directly with their CPA to determine exactly how the $2,560,000 deduction limit applies to their specific financial profile. Once you know your numbers, get your capital strategy lined up before Q4 ends so you can execute your purchases, place the equipment in service, and scale your business seamlessly.