For macroeconomic strategists and business founders alike, the Federal Reserve releases one of the most critical indicators of institutional liquidity every quarter: the Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS). The recently published April 2026 report reveals a distinct shift in how banks are deploying capital to businesses. For founders seeking to scale, understanding the data inside this document is the difference between securing necessary growth capital and hitting a brick wall of institutional friction.

This masterclass explores exactly how institutional banks operate behind closed doors, what changing economic data means for your commercial funding applications, and how you can position your enterprise to survive tightening credit markets.

Decoding the Data: What “Tightening Lending Standards” Actually Means

When the financial media reports that banks are “tightening lending standards,” it can sound like vague economic jargon. However, the Federal Reserve defines this tightening through two very distinct mechanisms of commercial underwriting: the extensive margin and the intensive margin.

The extensive margin refers to the bank’s baseline standards—whether they will approve an application at all. The intensive margin refers to the actual terms and conditions included in the loan contracts that they do approve.

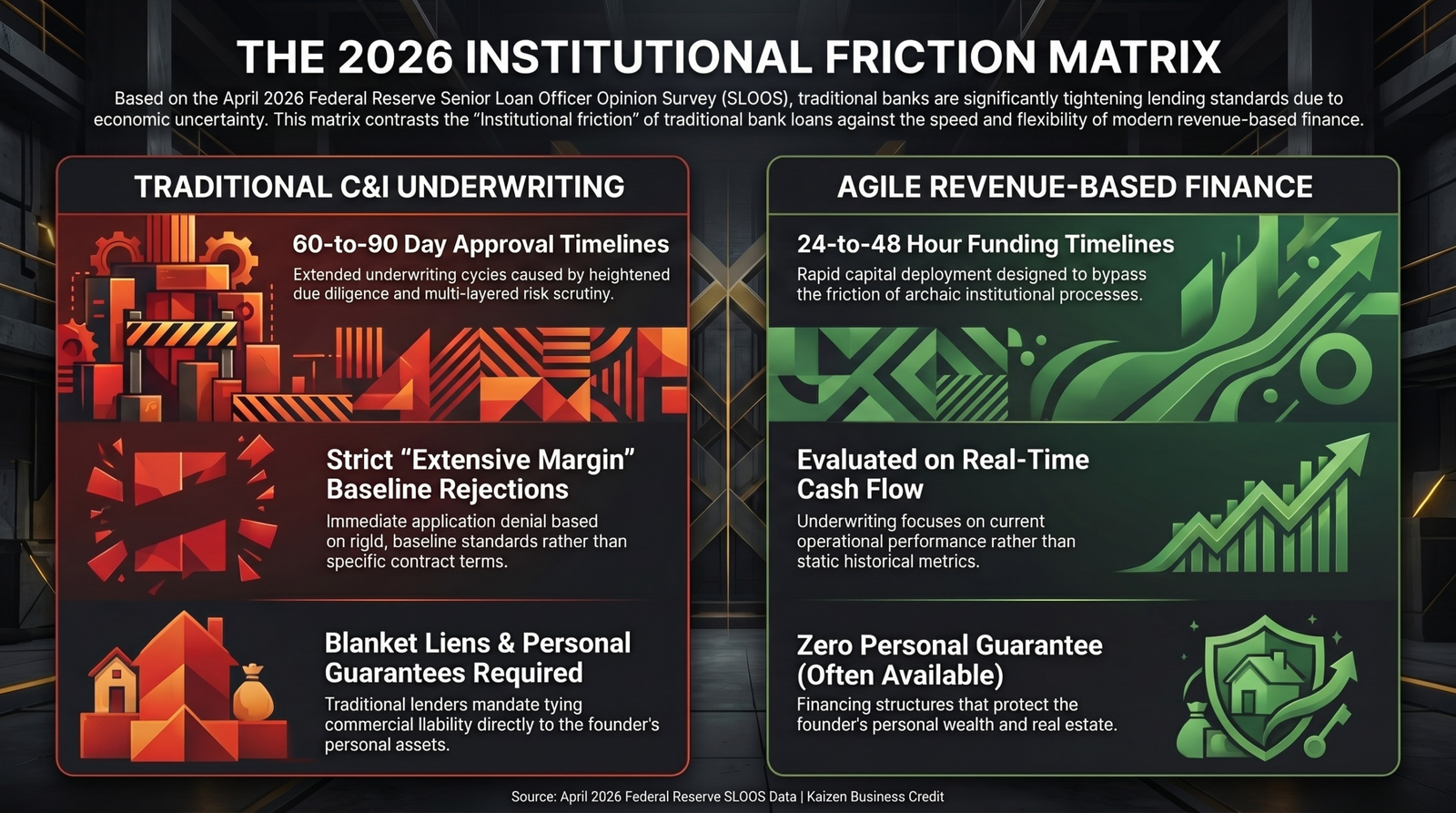

According to the April 2026 survey, a modest net share of banks tightened their baseline standards for Commercial and Industrial (C&I) loans across firms of all sizes. More importantly, banks reported tightening the actual terms of these loans. For a founder, this translates into immediate, real-world friction, manifesting as:

- Higher Premiums on Riskier Loans: Banks reported charging more for capital if a borrower’s profile is not flawless.

- Tighter Loan Covenants: Underwriters are instituting stricter operational and financial rules that your business must strictly adhere to during the life of the loan.

- Stricter Collateralization Requirements: Banks are demanding more physical or personal assets to secure and back the capital they lend.

The Mechanics of C&I Underwriting During Economic Shifts

Why do banks suddenly change their rules and make capital harder to access? The April 2026 SLOOS explicitly outlines the catalysts driving these boardroom decisions.

Among the banks that reported tightening their standards and terms for C&I loans, major net shares cited three primary factors: a “less favorable or more uncertain economic outlook,” the “worsening of industry-specific problems,” and a broadly “reduced tolerance for risk”.

Banks are risk-averse entities. When their economic visibility drops or they perceive storm clouds in specific industries, they react by building a fortress around their balance sheets, shifting the burden of risk directly onto the business owner.

Understanding Institutional Friction: Why Banks Move Slow

It is vital for founders to understand that traditional banks are not intentionally trying to stifle your business’s growth. They are heavily regulated institutions managing complex, highly scrutinized risk portfolios. We must examine the friction, not attack the institutions.

When a bank’s risk tolerance drops due to an uncertain economic outlook, they compensate by drastically increasing their due diligence. This explains the archaic 60-to-90-day underwriting processes that founders frequently endure. As underwriters are forced to scrutinize every financial metric, tax return, and revenue projection against a backdrop of macroeconomic uncertainty, approval timelines inevitably stretch.

Furthermore, this protective environment is exactly why traditional banks enforce stringent collateralization requirements and mandate strict personal guarantees. If the bank perceives a higher baseline of risk in the broader economy, they offset that exposure by tying the commercial liability directly to the founder’s personal real estate and personal assets. This ensures the institution has a guaranteed recovery mechanism if the business falters during an economic downturn.

Stress-Testing Your Balance Sheet

Knowing that banks are elevating premiums and tightening terms, founders must proactively stress-test their operations before applying for traditional C&I loans. To prepare for banking friction, you must view your business through the lens of a senior loan officer:

- Evaluate Your Collateral: Do you have the necessary unencumbered hard assets to meet the “tighter collateralization requirements” banks are currently enforcing?

- Review Margin Resilience: If a bank applies a higher risk premium or utilizes an interest rate floor on your credit line, can your operational cash flow comfortably sustain the higher cost of capital?

- Prepare for Strict Covenants: Ensure your accounting is pristine. With banks tightening loan covenants, traditional lenders will enforce rigorous, ongoing monitoring of your financial ratios.

By understanding the macroeconomic drivers behind bank behavior, you can accurately anticipate underwriting hurdles, optimize your balance sheet, and navigate the commercial credit markets like an institutional insider.

Desk Note: While understanding traditional bank mechanics is essential, high-revenue founders looking to bypass these tightened standards and institutional friction do not have to wait 90 days. You can secure revenue-based capital from $10,000 to $5 Million in 24 to 48 hours, often with Zero Personal Guarantee.