Some of the most successful commercial enterprises in the country started with a shaky personal credit score and a massive operational vision.

Unfortunately, traditional banking hasn’t caught up to that reality. When a local credit union or a big-box bank sees a founder’s FICO score dip below 680, they shut the door before the conversation even begins. They don’t care that your commercial roofing company just signed a $200,000 contract, or that your trucking fleet is billing $50,000 a month. To them, you are just a number on a credit report.

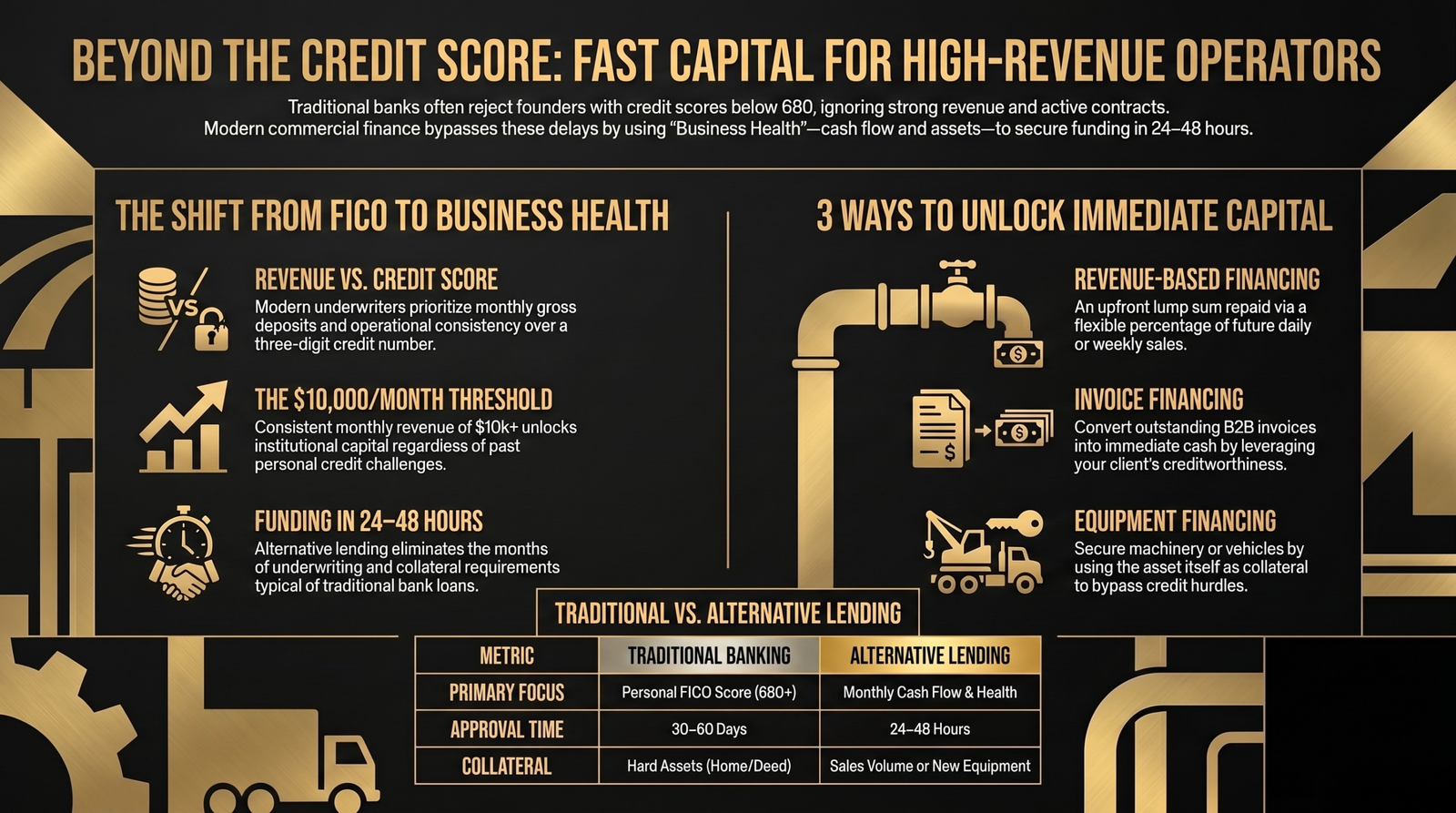

But in modern commercial finance, your credit score is no longer the gatekeeper to your growth.

If your business is generating consistent revenue, you have immediate access to institutional capital—regardless of past credit challenges. Here is the operator’s guide to securing fast, reliable business funding when traditional lenders say no.

Why Traditional Banks Say No (And Why It Doesn’t Matter)

Traditional banks operate on outdated risk models. They require pristine personal credit, heavy collateral (like the deed to your house), and months of underwriting just to offer a small term loan.

Alternative commercial lending operates on a completely different metric: Business Health.

Modern underwriters care about cash flow. They look at your monthly gross deposits, your time in business, and the consistency of your operations. If your business is breathing, moving, and making money, your personal credit score becomes a secondary (or even irrelevant) factor.

3 Fast-Funding Alternatives for Credit-Challenged Founders

If you have a low credit score but strong monthly revenue (over $10,000/month), you can access funding in 24 to 48 hours using these three alternative vehicles:

1. Revenue-Based Financing (The Cash Flow Play)

This is the fastest and most flexible way to get funding when credit is an issue. Instead of a traditional loan with fixed, rigid monthly payments, you receive an upfront lump sum of capital. The repayment is structured as a small, fixed percentage of your future daily or weekly sales.

- Why it works for bad credit: Approval is strictly based on your recent bank statements and sales volume, not your FICO score.

- The Advantage: If you have a slow week, your payment automatically adjusts down. It protects your cash flow when things get tight.

2. Invoice Financing (The Net-90 Solution)

If you run a B2B operation—like a trucking company, a construction firm, or a staffing agency—you know the pain of waiting 30, 60, or 90 days for a client to pay an invoice. Invoice financing allows you to sell those outstanding invoices to a lender for immediate cash.

- Why it works for bad credit: The lender doesn’t care about your credit score; they care about the creditworthiness of the client who owes you money.

- The Advantage: You unlock your trapped capital immediately without taking on traditional debt.

3. Equipment Financing (The Asset-Backed Move)

If you need a new dump truck, heavy machinery, or restaurant ovens, but your credit is stopping you from getting a bank loan, Equipment Financing is the answer.

- Why it works for bad credit: The equipment itself serves as the collateral for the funding. Because the lender’s risk is secured by the physical asset, they are highly forgiving of low personal credit scores.

- The Advantage: You get the machinery you need to generate revenue immediately, while spreading the cost out over 12 to 60 months.

The Kaizen Advantage: Speed Over Red Tape

When you are managing payroll, buying bulk materials, or fixing a broken piece of equipment, you do not have 60 days to wait for a bank to review your tax returns. You need capital now.

At Kaizen Business Credit, we bypass the traditional hurdles. We focus on the actual health and potential of your business, not a three-digit number from a credit bureau.

If you have been in business for at least 4 months and generate $10,000+ in monthly revenue, we can secure your capital.

Stop letting a credit score dictate your growth. Apply today. Submit a simple 1-page application and your last 4 months of business bank statements, and see your funding options in hours.